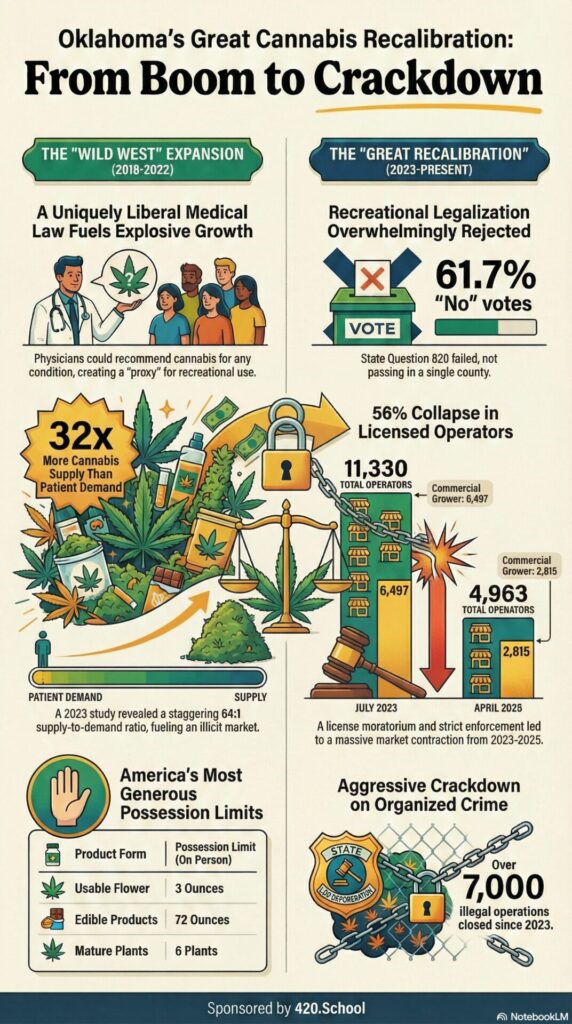

The “Sooner State” currently occupies a singular and frequently contradictory position within the American cannabis landscape. Since the historic passage of State Question 788 in 2018, Oklahoma has maintained one of the most accessible medical marijuana programs in the nation—one so permissive it effectively functions as a recreational market in all but name. Paradoxically, this same conservative electorate has decisively and repeatedly rejected “100% legalization” at the ballot box. As we navigate the “Great Recalibration” of 2025–2026, Oklahoma is transitioning from an era of unfettered, “Wild West” expansion into a period defined by aggressive regulatory consolidation and an unprecedented enforcement crackdown.

1. The “Medical” Market that Functions Like Adult-Use

Oklahoma’s medical framework is a global outlier. Unlike other states that require a specific diagnosis of terminal illness or chronic pain, State Question 788 established a system of pure physician autonomy. This lack of restrictive gatekeeping created a “proxy” for adult-use legalization, leading to a surge in participation where nearly 10% of the state’s total population holds a medical license.

“The Oklahoma statute empowered board-certified physicians to recommend cannabis for any condition they deemed beneficial for the patient.”

This “Medical-Only Plus” model remains highly accessible in 2025. Under the “Alternative Patient Identification” protocol, patients who receive digital approval through the OMMA MedPortal can now use their approval email or digital status to purchase medicine immediately, bypassing the two-week wait for a physical card. Because any adult can obtain a license with relative ease, the political urgency for full recreational legalization has evaporated; many voters view the current system as a sufficient, albeit regulated, middle ground.

2. The 64:1 Math Problem (The Supply-Demand Crisis)

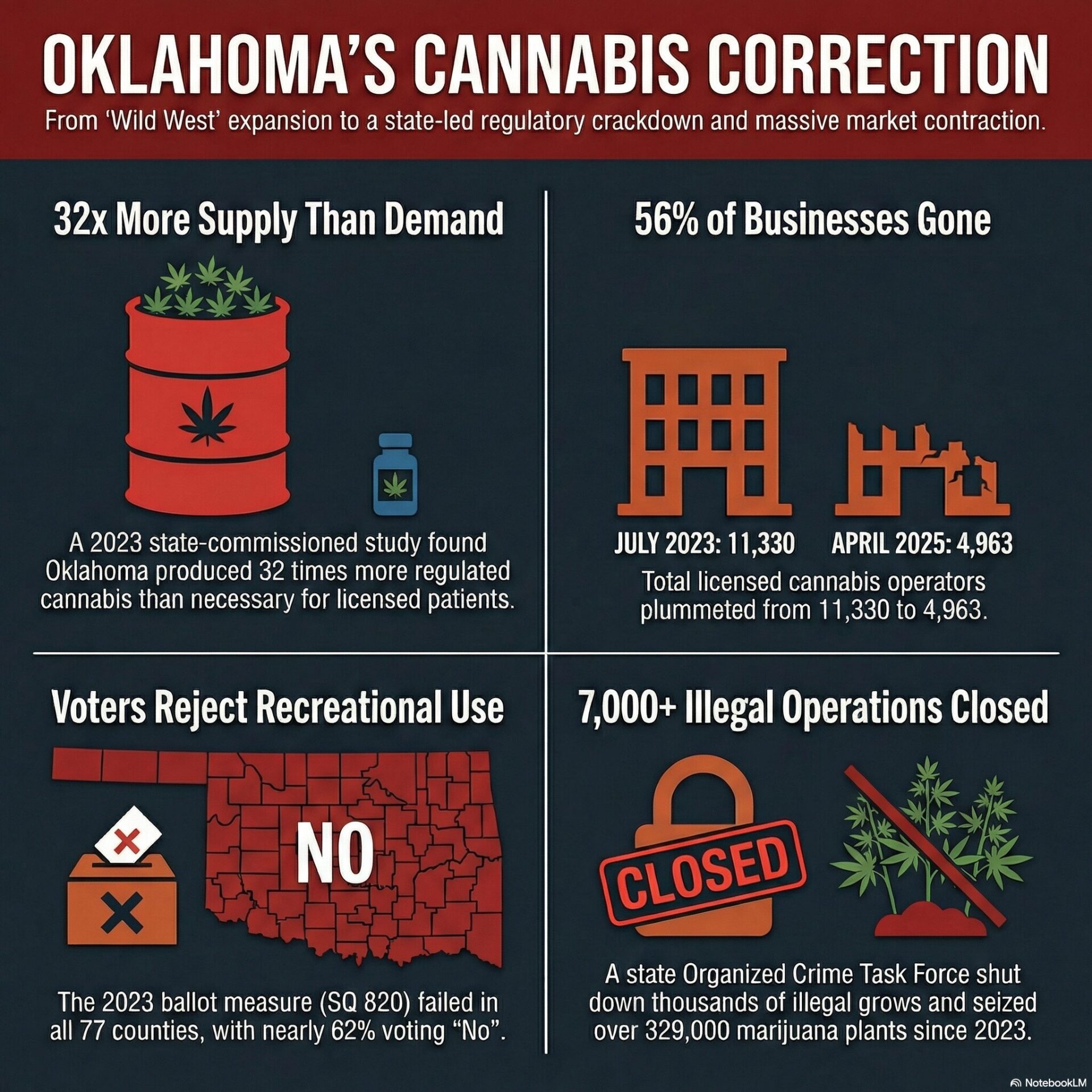

The primary driver of Oklahoma’s recent market instability was a staggering imbalance between production and actual patient need. A landmark 2023 study commissioned by the Oklahoma Medical Marijuana Authority (OMMA) revealed that the state was producing 64 grams of regulated cannabis for every 1 gram of actual patient demand. In a “healthy” market, a 2:1 ratio is standard; Oklahoma was operating with a 32x oversupply.

This glut caused wholesale prices to crater, with the US Cannabis Spot Index falling to a floor of roughly $888 per pound. This price collapse didn’t just hurt margins; it incentivized the mass diversion of product into the illicit export market.

| Market Metric | Finding / Standard |

| Oklahoma Supply Ratio | 64:1 |

| Healthy Market Standard | 2:1 |

| Total License Decline (July 2023 – April 2025) | -56.2% |

This “reckoning” triggered a brutal market contraction. Between July 2023 and April 2025, the total number of licensed operators plummeted by 56.2%, as the economic pressure of oversupply and rising compliance costs forced out non-compliant and undercapitalized “mom-and-pop” pioneers.

3. The “Wild West” is Being Tamed by Task Forces

The state has effectively declared war on the “Wild West” era. Led by Attorney General Gentner Drummond and the Organized Crime Task Force (OCTF), Oklahoma is aggressively purging the market of international criminal syndicates. This is no longer just a matter of regulatory paperwork; it is a high-stakes investigation into Chinese organized crime syndicates that have used “straw ownership” schemes to buy rural land. These syndicates have been linked to “execution-style killings” on illegal farms and the use of carbofuran—a banned, highly toxic pesticide—that threatens the state’s soil and water.

“By October 2025, the OCTF marked two years of success with staggering statistics: More than 7,000 illegal operations closed; 329,075 marijuana plants seized and destroyed; and 27 deportations of individuals linked to illegal grow operations.”

State leadership has made it clear that “managed contraction” is the only path forward. Through Senate Bill 212, which bars foreign nationals from acquiring title to Oklahoma land, the state is attempting to regain control of its landscape before the industry can be considered a stable, permanent fixture.

4. Taxes as a Fiscal “Anchor” for Public Schools

While social and religious opposition to cannabis remains high, the industry has become a vital component of Oklahoma’s fiscal health through the Redbud School Funding Act. This legislation creates a political “anchor” by tying the first $30 million in annual medical marijuana excise tax revenue directly to the State Public Common School Building Equalization Fund. This money is earmarked for the acquisition and maintenance of school buildings in under-funded and rural districts.

Current Tax Structure Breakdown:

- 7% Excise Tax: The primary levy on all dispensary gross receipts.

- 4.5% State Sales Tax: The standard state sales and use tax.

- Local Sales Tax: Varies significantly by municipality.

- Tulsa: Total tax burden of approximately 15.517% (including 8.517% local/state sales tax).

- Oklahoma City: Total tax burden of 15.75%.

Because these funds now support essential public education infrastructure, dismantling the industry would create a massive budgetary hole that few legislators are willing to defend.

5. The “Permanent Cap” and the End of the Land Rush

The era of easy entry is officially over. In 2026, the state is moving to replace its temporary licensing moratorium with a hard, permanent limit. House Bill 3144 proposes a statewide cap of just 2,550 grower licenses. With active growers having already fallen from nearly 6,500 in 2023 to roughly 2,800 by mid-2025, this legislation effectively freezes the market at its current consolidated level.

Furthermore, a new pre-packaging mandate (effective June 2025) has ended the “deli-style” model where flower was weighed at the counter. All products must now be pre-packaged by growers and processors in child-resistant, opaque containers. While intended to enhance safety, it has forced higher overhead costs onto small operators and sparked industry concerns regarding “mold bloom” in sealed, non-climate-controlled environments. This shift rewards only the most compliant, vertically integrated players who can survive the high costs of professionalization.

The Future of “Medical-Only Plus”

As 2026 unfolds, Oklahoma has established a unique “Medical-Only Plus” model. It offers near-universal access through a physician-led lens while maintaining a firm legal and cultural wall against 100% recreational legalization. The market is no longer defined by expansion, but by a “flight to quality” and rigorous policing.

By maintaining high possession limits and broad medical access while aggressively weeding out organized crime and illicit actors, the Sooner State is attempting a middle-path few other states have dared. Could Oklahoma’s “Medical-Only Plus” model—with its emphasis on physician autonomy and strict commercial caps—actually provide a more stable long-term path than the volatile, price-collapsing recreational models seen in states like Oregon or Michigan?