1. The End of the “Homeless Consumer” Era

The first wave of cannabis legalization was a logistical grind focused on supply chain mechanics: cultivation quotas, seed-to-sale tracking, and the clinical transaction of retail. As the industry enters its “second wave,” the narrative has shifted from the product to the place. This evolution into social consumption is not a luxury—it is a strategic necessity to solve the “homelessness of the consumer.”

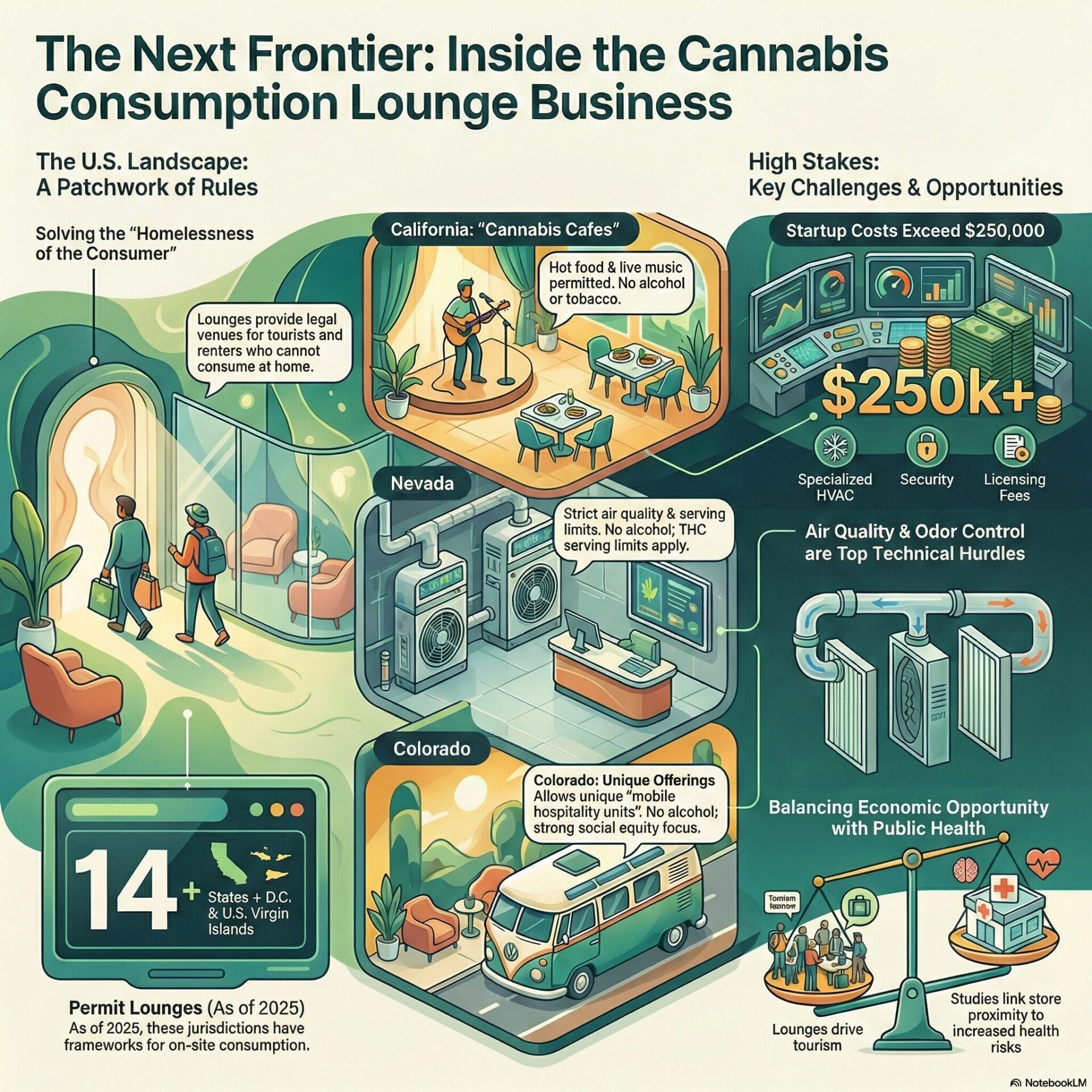

The industry currently operates in a regulatory vacuum created by a fundamental paradox: an adult can legally buy a gram of flower or a high-potency concentrate but has no legal place to ignite it. Public consumption remains a magnet for citations, and for the millions living in multi-unit housing or traveling as tourists, “legal” cannabis remains a contraband activity behind closed doors. This friction has created a legislative whiplash, forcing regulators to finally address the vacuum they created.

Alaska’s 2018 experiment broke the regulatory seal, pioneering the shift from treating lounges as stand-alone outposts to “retail endorsements”—essentially a hospitality add-on to an existing license. While this provided the initial blueprint, the subsequent response across the United States has evolved into a high-stakes regulatory gauntlet where a business’s survival depends entirely on its ability to navigate a patchwork of local “opt-in” ordinances.

| State | Primary License Type | Indoor Smoking Allowed | Food/Alcohol Policy | Local Control |

|---|---|---|---|---|

| Alaska | Retail Endorsement | Yes (with ventilation) | Food and non-alcoholic beverages allowed; No alcohol 6 | Municipal opt-in required 6 |

| California | Retail/Micro Endorsement | Yes (per local rule) | Hot food/non-alcoholic bev allowed (AB 1775); No alcohol or tobacco 5 | Municipal opt-in required 7 |

| Colorado | Hospitality & Sales | Yes (per local rule) | Food allowed; No alcohol 6 | Municipal opt-in required 5 |

| Dist. of Columbia | Safe Use Endorsement | Not Specified | Purchased on-site only 5 | District-wide 1 |

| Illinois | Dispensary/Tobacco Shop | Yes | Prepackaged food only; No alcohol 6 | Municipal opt-in required 6 |

| Maryland | Designated-Use Cafe | Outdoor Only | Single-serving edibles/bev allowed; No alcohol 5 | Municipal opt-in required 6 |

| Michigan | Designated Consumption | Yes | Food preparation allowed; No alcohol 6 | Municipal opt-in required 6 |

| Minnesota | Microbusiness/Hemp Retail | No (Infused food/bev only) | Food allowed; Alcohol permitted at hemp retailers only 6 | Municipal opt-in for events 6 |

| Nevada | Retail & Independent | Yes (sealed rooms) | Food allowed; No alcohol 11 | Municipal approval required 11 |

| New Jersey | Retail Endorsement | Yes | Delivery food only; No alcohol or tobacco 4 | Municipal approval required 1 |

| New Mexico | Retail Endorsement | Yes | Food allowed; No alcohol 6 | Municipal opt-in 1 |

| New York | On-site Consumption | Yes | Regulations pending 1 | Municipal opt-in required 1 |

2. The US Regulatory Patchwork: A Strategic State-by-State Comparison

The “municipal opt-in” model is the defining—and most frustrating—feature of the American landscape. This fragmentation creates a minefield for national operators; a profitable model in one zip code can be a criminal enterprise in the next. Yet, for the well-capitalized, this local control offers a “moat” around high-traffic urban centers.

To navigate this gauntlet, operators must decode a state-level matrix that defines everything from what you can smoke to whether you can serve a sandwich.

These archetypes—ranging from permanent lounges to temporary event permits—dictate a venue’s risk profile. While “on-site endorsements” offer a lower CAPEX for existing retailers, they often limit the “experience-first” hospitality that is currently revitalizing urban downtowns.

3. From “Retail-Plus-Couch” to Gourmet Hospitality: The California and Colorado Models

California is leading the charge in using cannabis as a tool for urban revitalization. The passage of Assembly Bill 1775, effective January 1, 2025, effectively killed the “retail-plus-couch” era, ushering in authentic “Cannabis Cafes.” By permitting live music, ticketed events, and—crucially—hot food, Sacramento is betting on cannabis to drive the foot traffic that post-pandemic downtowns so desperately lack.

The “premier destination” effect is best seen in West Hollywood (WeHo). Utilizing a merit-based licensing system that favored design-forward concepts over simple retail, venues like The Artist Tree have integrated high-impact art and open-air patios to create a hospitality landmark. This is no longer about selling a pre-roll; it is about selling a $50-per-head social experience.

Conversely, Colorado has leaned into mobile hospitality. Since 2023, Denver has authorized “mobile hospitality units”—essentially consumption lounges on wheels. The regulatory friction here is technical: driver compartments must be hermetically sealed and independently ventilated from the passenger area to prevent impairment. While California builds downtown anchors, Colorado is mobile-testing the limits of the tourism market.

4. The Technical Barrier: Ventilation, Public Health, and the Nevada Gold Standard

The true barrier to entry in the lounge sector is not the license fee—it is the mechanical engineering bill. Nevada has set the “Gold Standard” for technical compliance, mandating that smoking rooms be fully sealed with independent HVAC systems. To stay legal, these systems must achieve 8+ air changes per hour and maintain negative pressure to ensure no odor escapes the premises.

This “HVAC overkill” is the industry’s response to a “Public Health Paradox.” While lounges remove consumption from the streets, they concentrate indoor pollutants. California studies show that on-site vaping/dabbing can spike PM2.5 particulate matter levels 28 times higher than baseline. More alarming for policymakers is a 2025 Washington study found that those under 21 living near shops are 13% more likely to receive a Cannabis Use Disorder (CUD) diagnosis, compared to a 7% increase for adults.

For the operator, the labor friction is equally intense. Cal/OSHA now requires respirator masks and regular health screenings for employees. These are not mere safety suggestions; they are high-cost operational hurdles that can make or break a facility’s margin.

5. The Economic Calculus: Startup Capital, ROI, and the 280E Trap

Opening a consumption lounge is a capital-intensive bet with a path to profitability littered with tax traps. For a 3,000-square-foot facility, the initial CAPEX is daunting.

Pro Forma: Estimated Initial Investment for a 3,000 sq ft Facility

| Expense Category | Estimated Cost |

| Licensing, Legal Fees, and Insurance | $50,000 |

| Rent and Deposit | $100,000 |

| Space Improvements ($50/sq ft) | $150,000 |

| Security and Surveillance System | $65,000 |

| Furniture and Business Equipment | $50,000 |

| Marketing and Advertising (3-5% of sales) | $25,000 |

| Total Estimated Initial Investment | $447,000+ |

The “silent killer” of the lounge business is Internal Revenue Code Section 280E. Because the federal government still classifies cannabis as a controlled substance, lounges cannot deduct standard operating expenses—only the “cost of goods sold.” While some states allow state-level deductions (potentially bumping margins from 10% to 21%), the federal burden remains a primary obstacle to scalability.

In tourism-dependent hubs like Atlantic City, operators face a brutal seasonality. Revenue can plummet by 35% during winter months, forcing businesses to burn through cash to maintain the high fixed costs of “Nevada Gold Standard” ventilation systems on a Tuesday in February.

6. Social Equity vs. Operational Liquidity: The Implementation Gap

There is a widening chasm between the social intent of equity programs and the brutal reality of the “Operational Liquidity Trap.” While states prioritize applicants from communities impacted by the War on Drugs, the capital requirements act as an unofficial gatekeeper.

- Nevada’s Failure: Despite a 50% set-aside for independent equity licenses, zero venues had opened by mid-2025. The culprit? A $200,000 liquidity requirement and a total absence of traditional banking.

- New Jersey’s “Capital-First” Pivot: New Jersey has attempted to bridge the gap with $250,000 Joint Venture Grants, recognizing that a license without capital is merely a piece of paper.

- New York’s Banking Push: The state has enlisted credit unions like Suffolk and Ponce Bank to solve the capital access problem, though the $450,000+ build-out cost remains a high bar for most.

7. Global Divergence: From Thai Recriminalization to the European Club Model

Internationally, the market is swinging from “wild west” expansion toward strict medicalization or non-profit associations.

Thailand serves as the “Great Regulatory Reversal.” After a brief period of unregulated growth, the government re-classified flower as a “controlled herb” in June 2025. Over 7,000 shops shuttered almost overnight. Under the 2026 framework, any purchase of flower requires a Thai medical prescription, ending the era of the casual tourist lounge.

Europe, meanwhile, is rejecting the commercial retail model in favor of Non-Profit Social Clubs.

| Country | Key Model | Home Growing Limit | Personal Consumption |

| Germany | Non-profit clubs; no commercial retail | 3 plants | Legal (Private/Public limits) |

| Malta | Non-profit Associations (CHRAs) | 4 plants | Legal (Private) |

| Netherlands | Regulated “coffeeshop” experiment | 5 plants (tolerated) | Tolerated |

| Spain | Private Cannabis Social Clubs | Tolerated | Decriminalized (Private) |

In Canada, provincial inertia continues to stall the market. Major hubs like Ontario and British Columbia still lack a federal framework for lounges, forcing entrepreneurs into “gray area” solutions like Alberta’s MaryJane Manor, which bypasses rules by physically separating the hotel lounge from the licensed retail store.

8. The Final Frontier of Legalization

Consumption lounges represent the final stage of cannabis normalization, moving the plant from a hidden transaction to a structured social experience. The sector’s future is pinned to a late-2025 Executive Order expected to expedite rescheduling to Schedule III, which would finally dismantle the 280E tax trap. As consumer habits shift toward beverages and high-end edibles, the “smoking den” will likely be replaced by wellness retreats and sophisticated hospitality suites.

Survival Imperatives for Stakeholders:

- Technical Hedging: Hedge against future litigation and citation by exceeding Cal/OSHA and Nevada air quality standards from day one. HVAC is not a place to cut corners.

- Labor Friction Mitigation: Implement aggressive staff training on impairment detection and safe service. In an era of respirator mandates, employee health is an OPEX priority.

- Legislative Guerrilla Warfare: Operators must engage in local advocacy to shape municipal “opt-in” rules. If you are not at the table to define what constitutes a “cannabis cafe,” you will be regulated out of existence before you open.

The integration of these venues into the modern urban landscape is inevitable, but only for those who can survive the financial and regulatory gauntlet of the social frontier.